The AtwoB Report - 2nd Quarter 2018

Our economic analysis, market commentary and key takeaway for the previous quarter.

The U.S. economy has been growing for 9-years. Unemployment is historically low. In fact, at 4%, it hasn’t been lower since 1969. Second quarter economic activity is looking particularly strong. The Atlanta Fed’s latest GDPNow forecast stands at a robust 4.1%. If the economy grows for another 12-months, we will have entered the longest uninterrupted stretch of growth in U.S. history. Job growth continues to be robust and wages are increasing as well. On top of this, tax cuts and government spending, approved in the fourth quarter of last year, are expected to continue to work their way through the economy. Not much to complain about here. The present economic picture looks good.

And yet, for the first time in a long time, whispers of the “R-word” have started to float around. The “R-word” is a recession, or a slowdown in economic growth whereby the economy contracts for a period instead of expanding. While most current and leading indicators are not forecasting a deceleration imminently or even in the next year or so, some economists are looking out to the end of 2019 and 2020 as a time where this long expansion may meet its demise. So what gives? If the economic backdrop is so strong in the U.S. currently, why might we begin to think that a recession may not be too far off?

The answer, as most answers tend to be when dealing with markets and economies, is counterintuitive. The reason why it’s fair to assume that a recession is a growing possibility is precisely that the economy is strong. This excerpt from the minutes of the latest Federal Reserve meeting begins to explain why:

“Some participants raised the concern that a prolonged period in which the economy operated beyond potential could give rise to heightened inflationary pressures or to financial imbalances that could lead eventually to a significant economic downturn”

FedSpeak Translation: The Federal Reserve is concerned that if the economy “overheats” it can lead to higher prices and financial “bubbles”, both of which can have a substantial adverse economic impact the longer those balloons inflate and eventually pop.

As mentioned above, the U.S. economy is quite strong and up until recently, the global economy has been growing in a wonderfully synchronized way. However, this strength has now led to the point where an extremely supportive monetary policy is no longer necessary and indeed needs to be unwound, both here and abroad. The experience of leaving rates too low for too long cannot be far from the Fed’s collective consciousness, as they often receive blame for helping to promote the real estate bubble that precipitated the Great Recession. Now, the Federal Reserve is looking to find the place where interest rates are neutral and neither support overheating or contracting. Easier said than done when trying to manage the vagaries of an extraordinarily complex and dynamic domestic and interconnected global economy. The markets are now taking notice and focusing on the less certain future of the economy, as opposed to the strength in the present.

Fear the Curve?

One particular indicator that has many concerned is what is known as the yield curve of the bond market. The yield curve represents all of the different bond maturity levels of the US Treasury bond curve, from very short (3-months) to very long (30-years). A typical yield curve is upward sloping, because investors will demand higher yields for holding bonds for a longer time. But from time to time, the upward shape of the yield curve does not keep, and the curve inverts. An inverted curve means that short-term rates are higher than long-term rates, as investors believe that both economic growth and inflation may be lower in the future, and therefore demand less compensation in the form of lower yields. The yield curve is monitored closely because every recession going back to 1975 was preceded by the yield curve inverting. And, following five of the past six periods in which the yield curve inverted, the economy tipped into recession within a year, according to data from the St. Louis Fed.

Why does this matter now? As of July 5th, the gap between short and long yields has moved to 11-year lows as the yield curve has flattened significantly. The difference between 2-year yields and 10-year yields is only 0.28%. Remember 11-years ago? It was 2007. The aftermath was unpleasant. If the Fed continues to raise short-term interest rates as expected and longer-term rates don’t move higher, an inversion of the curve may not be far off. Many believe that this time may be different and are not concerned about the signal. Maybe they are right. Long-bond yields may still be lower than they should be given the unorthodox global monetary policy of the last 10-years. That said, we’re always wary of the words “this time is different” and will continue to pay close attention to this indicator.

(Trade) War. What is it Good For?

We’ll find out. Because it appears that we’re in one. As of July 6th, the U.S. has imposed tariffs on $34 billion of Chinese imports, with China immediately responding in-kind. These tariffs follow on those that the U.S. has imposed on steel and aluminum imports from the European Union, Canada and Mexico. The EU has already retaliated by placing tariffs on U.S. bourbon and Harley’s. This type of tit-for-tat trade activity has not occurred for some time as a long movement towards a more globalized economic order has been placed on hold. The ultimate results of this type of trade-war are yet to be known, but a recent economic analysis by the Bank of England suggests that raising tariffs by ten percentage points between the US and its major trading partners will reduce U.S. GDP by 2.5% over three years and reduce aggregate global GDP by 1%. The unquantifiable risk in all of this is the uncertainty it creates for corporations and global markets as global trade has already cooled significantly before the tariffs. There will of course be relative winners and losers in all of this, and some necessary adjustments are needed relative to the trade parameters with individual countries such as China, but if the global economic pie ends up contracting as a result of uncertainty or a trade war gone too far, it may be difficult to figure out what the war is good for.

Market Impact

The observable impact on the markets has been an increase in market volatility with little return to show for it in 2018. US stocks have eked out a small gain, viewed as the relative safer bet with a stronger economy so far this year compared to many others. As the Fed has increased rates, the US dollar has also gained in strength relative to other global currencies. The higher value of the dollar has put a dent in international market returns, particularly those in the more sensitive emerging markets, where dollar strength can make paying back dollar-denominated debt more difficult. For a globally diversified investor, a premise in which we believe in, global market returns have been essentially zero in 2018. Bonds struggled mightily early in the year, but have steadied as of late in the face of more uncertainty. That said, bond returns are also down so far this year.

Just like the strength in the economy, present corporate conditions can scarcely be much better. According to the latest from Factset, “The estimated (year-over-year) earnings growth rate for Q2 2018 is 20.0%. If 20.0% is the final growth rate for the quarter, it will mark the second highest earnings growth reported by the index since Q3 2010 (34.0%), trailing only the previous quarter (24.8%). It will also mark the third straight quarter in which the index has reported double-digit earnings growth. All eleven sectors are expected to report year-over-year growth in earnings. Seven sectors are expected to report double-digit earnings growth, led by the Energy, Materials, Telecom Services, and Information Technology sectors.”

The results for corporate America have been pretty stellar so far this year, but market returns have seriously pumped the breaks. Again, it pays to think counterintuitively to explain why this may be happening.

When conditions are very good, as they seem to be now from both an economic and an earnings perspective, it might lead us to think that markets should concurrently be strong. But markets don’t typically live in the present, instead they try and discount what will happen in the future. Markets don’t usually go down after a recession hits, they typically begin to decline well ahead of a potential slowdown. Earnings are robust now, but markets ponder whether we will look back a year from now and say things peaked already. So as we sit here at the mid-way point in 2018, here are the questions markets will have to deal with going forward:

- Will the Fed tighten the screws on the economy to prevent it from overheating and can they engineer a “soft-landing” of not too hot and not too cold economic growth?

- If not, when may we see the next “R-word”?

- Will the inversion of the yield curve, a typically reliable indicator of economic slowdown happen? If so, is this time different?

- Will the “trade war” decrease global economic confidence or will it have a benign impact?

- How long can corporate earnings keep up the excellent work or has the earnings cycle peaked?

These questions all boil down to the same theme. Things are good now, but how long can they stay that way? Jeff Gundlach, manager of the Doubleline Total Return Fund and whom we believe to be as in-tune with the markets as any investor out there, may have summed it up best in one tweet:

“Yield curve nearly flat 2/10 + Fed auto-tightening + QT (quantitative tightening) + tariffs + high stock and bond valuations + exploding deficit =

Risk, not goldilocks.”

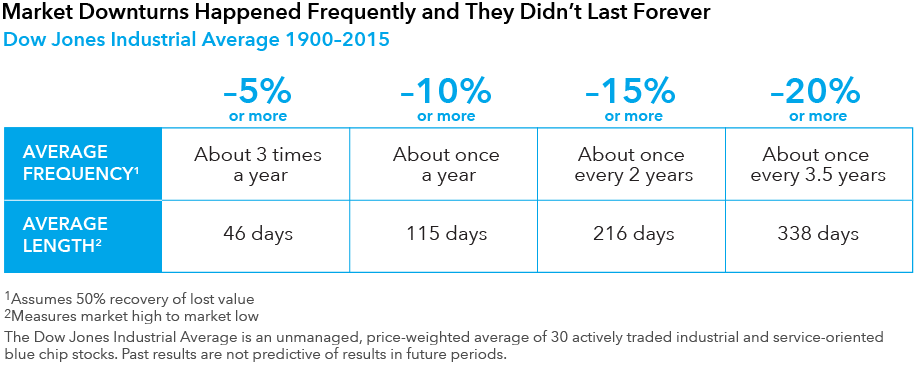

Markets will Be Markets

Our quarterly reminder of what normal market risk looks like, courtesy of Capital Group/American Funds:

The Key Takeaway

The U.S. economy and corporate earnings are currently in a great place. But markets care less about today than they do tomorrow. The grind of more risk and lower market returns so far this year likely reflect a contemplation of whether this is as good as it gets. If it is, we should expect more volatility, returns that are more difficult to come by, and the possibility of normal market downturns that feel harsher given how benign conditions have been for so long. As we often note, your portfolios seek to withstand both your personal ability to handle negative swings in the market and your financial plan’s ability to withstand less fruitful investment environments. We would love to think that markets will keep chugging along, but we will always be mindful of the potential shifts in the wind and what that means for your plan. We believe, our conservative approach to planning for the future and projecting future returns helps to embed a potential margin of safety into your financial plan, but we will always be mindful of how actual conditions on the ground evolve, and will adjust portfolios and plans accordingly, and if needed.

Important Disclosure Information

This report is provided as information and commentary regarding the market. The views expressed in this report are as of the date of the report, and are subject to change based on market and other conditions. This report contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Past performance is not a guarantee of future returns. Investing involves risk and possible loss of principal capital. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by AtwoB, or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices.

Please note that nothing in this report post should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be, investment, accounting, tax or legal advice. If you would like investment, accounting, tax or legal advice, you should consult with your own financial advisors, accountants, or attorneys regarding your individual circumstances and needs. Advice may only be provided by AtwoB after entering into an advisory agreement. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from AtwoB. If you are an AtwoB client, please remember to contact AtwoB, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. AtwoB is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the AtwoB’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request.

If you have any questions regarding this report, please contact us at info@today2b.com or 914.302.3233.